As businesses enter 2026, payment activity in the Philippines is becoming more digital, more real-time, and more infrastructure-driven. The Bangko Sentral ng Pilipinas has already moved to align retail payment systems with the ISO 20022 standard, and it is also studying near-24/7 PhilPaSSplus operations to support faster and more continuous payment flows. For retailers and B2B merchants handling custom or high-value orders, this makes partial payments more relevant as customers look for more flexible ways to complete purchases.

At the same time, businesses are adjusting to tighter operating conditions linked to flexible work arrangements in the Philippines and shorter on-site schedules in some settings. In this environment, accepting a deposit is only part of the process. Companies also need to track remaining balances, reserve inventory accurately, and keep payment and accounting records aligned. This article explains how partial payments work and what businesses need to manage them more efficiently.

Key Takeaways

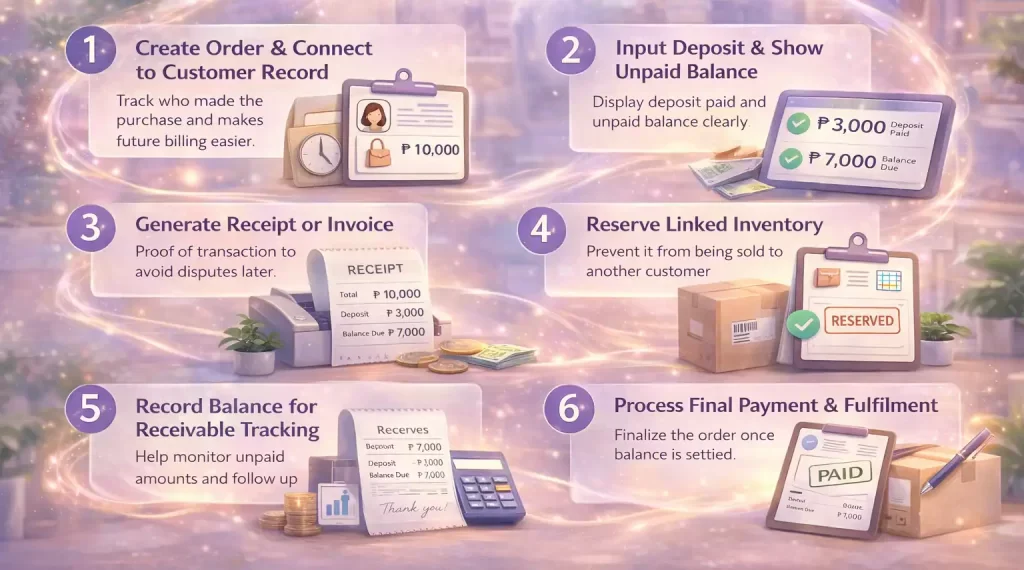

A partial payment is a payment arrangement where a customer pays only part of the total order value upfront, while the remaining balance is settled later based on agreed terms. This setup is common in custom orders, bulk purchases, pre-orders, and other transactions where businesses need a deposit before fulfilment. That is why partial payments should not be treated as a simple checkout feature. Once a business accepts a deposit, it must also be able to track the customer’s outstanding balance accurately, manage reserved inventory so stock stays aligned with the order, and keep payment records consistent with accounting reports. If these processes are not handled in one clear workflow, businesses can face collection delays, stock discrepancies, and reporting errors that disrupt operations and weaken customer trust. Handling partial payments requires more than simply accepting a deposit. Businesses also need to track the remaining balance, reserve inventory, and keep financial records accurate. For small business owners and accounting teams, a structured workflow can help reduce billing errors, prevent stock mismatches, and make final settlement easier to manage. In this context, a POS for small retail stores helps businesses track partial payments and manage the payment process seamlessly within their system. Step-by-step partial payment flow: Managing deferred payments at scale requires three things working in tandem: clear written policies, a POS system in the Philippines integrated with your accounting stack, and compliance with the legal and data security frameworks that govern how deposits and customer data are handled. Each layer builds on the next. Merchants should calculate the minimum deposit needed to cover costs and mitigate default risks. For custom orders, this includes raw material and labor costs, while for retail items, it covers restocking and holding fees. Deposits typically range from 20% to 50%, depending on margins. Every invoice that includes an outstanding balance must be accompanied by explicit terms and conditions. These terms must clearly articulate: POS systems should be integrated with accounting, CRM, and inventory to track payments, revenue, and stock levels. Real-time synchronization enables accurate financial tracking, while CRM automation sends reminders to customers, improving cash flow and reducing manual effort. Businesses must ensure secure handling of customer and payment data. Compliance with security protocols and clear terms reduces the risk of fraud and disputes. Proper systems protect sensitive information, ensuring data security and legal adherence. Managing partial payments effectively comes with its own set of challenges. Businesses must address the following struggles: The mechanics of partial payments are well established of what is changing is how intelligently businesses can manage them. AI, predictive analytics, and blockchain are moving from pilot projects into live POS environments, giving merchants tools to personalize payment terms, forecast cash flow with precision, and automate collections in ways that were not practical even a few years ago. Most businesses still apply the same deposit rule to every customer, even though payment risk can vary from one transaction to another. With AI integrated into the POS, businesses can assess customer history, purchase behavior, and risk factors more quickly to set more suitable payment terms. As a result, trusted customers may qualify for lower deposits, while higher-risk transactions can require stronger upfront payment to reduce default risk. Many businesses still monitor outstanding balances only after payments become overdue. With predictive analytics, POS and retail ERP systems can read past payment patterns to estimate when customers are likely to settle their balances. This helps finance teams plan cash flow more accurately and respond earlier to possible collection delays. Some B2B and high-ticket transactions still depend on manual invoicing and payment verification, which slows down collections. With smart contracts and blockchain, the payment terms can be recorded automatically when a deposit is made, and the final payment can be released once a set condition, such as delivery confirmation, is completed. This helps reduce manual follow-up and makes the payment process more secure and efficient. The mechanics are consistent, but the specifics vary by sector. Here is how partial payments play out across three of the most common use cases. Partial payments are no longer just a temporary solution. They have become a practical way for retail and B2B businesses to support more flexible transactions. When managed with clear policies, connected systems, and accurate recordkeeping, they can reduce purchase friction, improve order value, and strengthen customer trust. Businesses usually run into problems when deposits, balances, and accounting records are still handled manually. Partial payments need strong operational control, not just a flexible sales approach. Businesses must be able to manage deposit rules, track outstanding balances, and keep payment records aligned with inventory and accounting data. For companies reviewing this capability, exploring a POS system in the Philippines that supports partial payments and accounting integration can be a practical next step. Yes, WooCommerce can support partial payments through specific payment plugins or custom checkout configurations. This setup allows merchants to accept deposits or split payments, depending on how the store’s payment workflow is designed. Yes, businesses can accept partial payments with PayPal, but the setup usually depends on the platform, plugin, or payment integration being used. Merchants should also make sure the system can track the remaining balance properly after the initial payment is received. Amazon may support partial payment in certain cases, but the availability depends on the product, payment method, or promotional offer. For merchants, this is different from a direct partial payment setup in their own POS or e-commerce system, where they manage deposits and outstanding balances themselves. In online stores, partial payments usually allow customers to pay a deposit first and settle the remaining balance later. To manage this smoothly, the business needs a system that can record the initial payment, track the unpaid amount, and connect it to the correct order and customer record. HashMicro follows strict editorial standards and uses primary sources such as regulations, industry guidance, and trusted publications to keep content accurate and relevant. Chat Now : |