A general ledger is the main record used to organise and track a business’s financial transactions. It brings together information from sales, purchases, payments, and other accounting activities into a single system.

As transactions are recorded, they are assigned to specific accounts and used to build financial reports. This helps businesses monitor their financial position, review performance, and maintain accurate records over time.

Key Takeaways

A general ledger is the central accounting record used to organise and track financial transactions.

Transactions move from journal entries into ledger accounts before being used in financial reports.

General ledger accounts are grouped into assets, liabilities, equity, revenue, and expenses.

Accounting software automates posting, reconciliation, reporting, and ledger management.

What Is a General Ledger?

A general ledger is the central record used to organise and track a business’s financial transactions. Transactions are grouped into individual accounts, making it easier to monitor balances and financial activity.

Journal entries are first recorded and then posted to the general ledger, where account balances are continuously updated. The ledger also provides the data used to prepare key financial statements, including the balance sheet, income statement, and cash flow statement.

By keeping financial information organised and up to date, the general ledger supports accurate reporting, compliance, and day-to-day financial management. It also provides the foundation for budgeting, forecasting, and business decision-making.

This gives finance teams real-time financial visibility across account balances, transaction activity, and overall business performance.

How a General Ledger Works

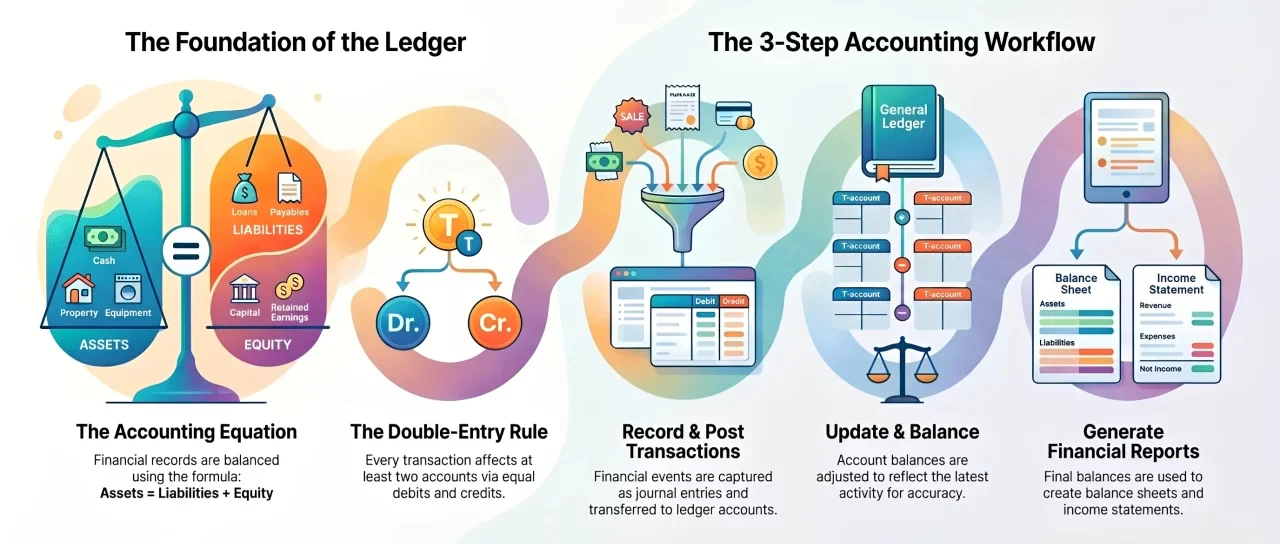

Every financial transaction follows a structured process before it appears in financial reports. The general ledger acts as the central record that collects, organises, and summarises these transactions.

1. Double-Entry Bookkeeping and the General Ledger

The general ledger operates using double-entry bookkeeping, where every transaction affects at least two accounts. One account is debited while another is credited by the same amount, helping maintain balanced financial records.

This approach follows the accounting equation:

Assets = Liabilities + Equity

For example, when a customer payment is received, one account increases while another decreases or records revenue. Recording both sides of the transaction helps maintain accuracy across the ledger.

This structure also supports tracking customer payments because each receipt can be matched to the correct account and transaction record.

2. From Journal Entry to Financial Statement

- Record the transaction

A financial event such as a sale, purchase, or payment is recorded as a journal entry. - Post to the ledger

The journal entry is transferred to the relevant accounts within the general ledger. - Update account balances

Each account balance is adjusted to reflect the latest financial activity. - Generate financial reports

Account balances are used to prepare reports such as the balance sheet, income statement, and cash flow statement.

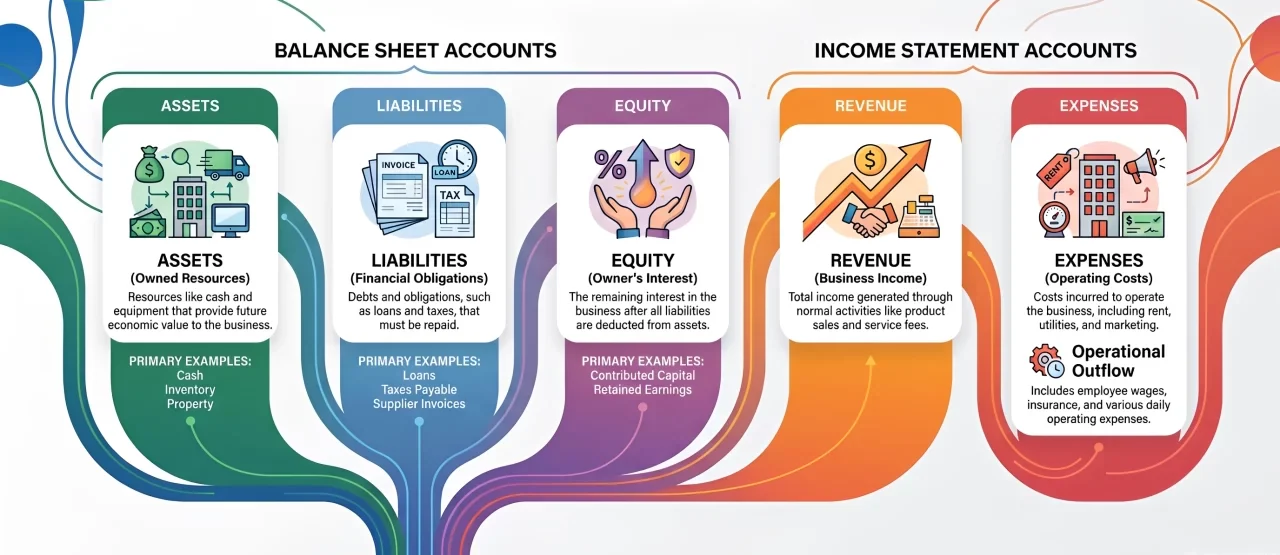

Five Types of General Ledger Accounts

The general ledger is organised into several account categories that help businesses classify and track financial transactions. Each account type serves a different purpose and contributes to accurate financial reporting.

1. Assets

Assets represent resources owned or controlled by a business that provide future economic value. Common examples include cash, inventory, equipment, property, and accounts receivable.

2. Liabilities

Liabilities record financial obligations that a business must repay in the future. These may include supplier invoices, loans, taxes payable, and employee-related obligations.

3. Equity

Equity represents the owner’s interest in the business after liabilities are deducted from assets. It typically includes contributed capital, retained earnings, and owner drawings.

4. Revenue

Revenue accounts track income generated through normal business activities, such as product sales, service fees, subscriptions, or project billings.

5. Expenses

Expense accounts record the costs incurred to operate the business, including wages, rent, utilities, insurance, marketing, and other operating expenses.

General Ledger Example

The example below shows how transactions are recorded and organised within a general ledger.

As transactions are posted, debit and credit entries update account balances and maintain accurate financial records. Clear ledger records also help with resolving account discrepancies when balances, payments, or transaction details do not match.

General Ledger vs General Journal

Although both are essential accounting records, the general journal and general ledger serve different purposes within the accounting cycle.

The journal records transactions first, while the ledger organises them into account balances used for reporting.

General Ledger Codes and the Chart of Accounts

General ledger (GL) codes are unique identifiers assigned to individual accounts within the chart of accounts. They help businesses categorise transactions consistently and ensure financial information is recorded in the correct account.

The chart of accounts provides a structured framework for organising assets, liabilities, equity, revenue, and expenses. It helps businesses categorise transactions consistently.

A logical numbering system improves reporting accuracy and makes financial data easier to manage. Most accounting software allows businesses to customise their chart of accounts to suit their reporting needs.

Common Chart of Accounts Structure

- 1000-1999 Assets: Cash, inventory, accounts receivable, and fixed assets.

- 2000-2999 Liabilities: Accounts payable, loans, taxes payable, and other obligations.

- 3000-3999 Equity: Owner’s capital, retained earnings, and shareholder equity.

- 4000-4999 Revenue: Sales income, service revenue, and other operating income.

- 5000-5999 Cost of Goods Sold: Direct costs associated with producing or delivering goods and services.

- 6000-6999 Operating Expenses: Rent, wages, utilities, marketing, and administrative expenses.

How Accounting Software Manages the General Ledger

Modern accounting software automates many of the processes involved in maintaining the general ledger. Transactions from invoices, bills, payroll, and other business activities can be recorded automatically, reducing the need for manual data entry.

The software supports bank reconciliation and updates account balances in real time. This helps maintain accurate records and makes financial reporting more efficient. These automated financial workflows help reduce repetitive tasks and keep ledger records updated across connected business processes.

Benefits of General Ledger Automation

- Reduced manual entry: Automatically records transactions from connected business processes.

- Improved accuracy: Minimises data entry errors and maintains consistent account coding.

- Faster financial reporting: Generates reports using up-to-date ledger information.

- Real-time visibility: Provides immediate access to current account balances and financial performance.

- Better audit readiness: Maintains organised records and a clear transaction history for compliance purposes.

Accounting software helps businesses automate general ledger management by connecting financial transactions across sales, purchasing, inventory, and payroll within an accounting system. Many accounting solutions for Australian business also support compliance reporting, reconciliation, and real-time access to financial data.

Conclusion

A general ledger serves as the central record for organising financial transactions and maintaining accurate account balances. It supports financial reporting, audit readiness, and informed business decision-making.

By combining structured account classifications with accounting software automation, businesses can improve accuracy, reduce manual work, and gain better visibility into their financial performance.

If you are looking to modernise your accounting processes, you can book a free walkthrough with our team to see how an integrated accounting system can support your financial management requirements.

Frequently Asked Question

A general ledger is the main accounting record used to organise and track all financial transactions within a business.

The five main account types are assets, liabilities, equity, revenue, and expenses.

A general journal records transactions chronologically, while a general ledger organises those transactions into individual account balances for reporting.

General ledger codes are unique account numbers used to classify transactions within the chart of accounts and improve reporting accuracy.

Yes. Accounting software can automatically record transactions, update account balances, perform reconciliations, and generate financial reports using real-time ledger data.

![Balance Sheet Template: Free Downloads for Businesses [2026]](https://stg-cms.hashmicro.com/uploads/blog-5780aa690704-moneymoney-14.webp)