Job costing tracks all costs associated with a specific project, contract, or job. It assigns labour, materials, and overhead to individual jobs so you can see exactly what each one costs to deliver.

This matters because profitability varies from job to job. A construction firm might earn strong margins on residential renovations but bleed money on commercial work. Without job costing, profitable work masks unprofitable work.

This article explains how job costing works, when to apply it, how to calculate it, and how Australian businesses across construction, manufacturing, and professional services use it to protect their margins.

What Is Job Costing?

Job costing is a cost accounting method that assigns direct and indirect costs to individual jobs, projects, or contracts. Each job gets its own cost record covering three categories: labour, materials, and overhead.

The method operates on a clear principle: when you know what each job costs to deliver, you can price accurately, catch unprofitable work early, and make informed decisions about which jobs to pursue.

Job costing is the direct counterpart to process costing, which averages costs across large volumes of identical output. It suits businesses where every project differs from the last, such as custom builds and client-specific contracts.

Why Job Costing Matters

Businesses that skip job costing rely on gut feel to judge profitability. Once you run multiple concurrent jobs with different scopes and cost structures, untracked costs erode margins without warning.

Job costing acts as an integrated system for financial tracking, giving you visibility into which jobs make money, where estimates fall short, and how to sharpen future pricing.

It also simplifies progress billing. When you know actual spend against the quoted amount, invoicing becomes a verification step rather than a guessing exercise.

For Australian businesses, this discipline is especially valuable given how common fixed-price contracts are in construction and professional services. A cost overrun on a fixed-price job comes straight out of margin with no mechanism to recover it.

When Should You Use Job Costing?

Job costing makes sense when your business delivers distinct, identifiable jobs rather than continuous production. Two questions clarify the fit.

- Is each job different?: If your output varies by client, scope, or specification, job costing captures the real cost of that variation. If every unit is identical, process costing is more efficient.

- Can you trace costs to a specific job?: If your team logs time against projects, your materials go to specific sites, and your purchase orders reference job numbers, the data infrastructure for job costing already exists.

Most construction companies, project-based manufacturers, and professional services firms answer yes to both. If you quote individual jobs and want to know whether each one made money, job costing is the right method.

Job Costing Use Cases

Job costing applies across any business that delivers distinct, project-based work. Three industries use it most consistently.

1. Construction companies

Construction is where job costing originated. Every project has a unique scope, timeline, and subcontractor roster. A builder tracking costs per project can compare actual spend against the original estimate and catch overruns as they develop.

Construction is one of Australia’s most economically significant industries. According to the Australian Bureau of Statistics, the sector employs around 1.3 million workers, making it one of the largest employing industries in Australia.

In Australia, job costing supports construction cost management by tracking labour, materials, subcontractor invoices, equipment hire, and site overhead.

For head contractors managing multiple active sites, it also creates the audit trail required under construction contracts and security of payment legislation.

2. Manufacturing Businesses

Custom manufacturers use job costing to price each production order on its own merits. The method captures direct materials consumed, machine time, and labour hours for a specific run.

Factory overhead is then applied at a predetermined rate. Where an order spans multiple shifts or departments, all costs are consolidated into a single job record rather than being lost over time.

This distinguishes job costing from process costing, which averages costs across continuous high-volume output. The two methods serve fundamentally different production models.

3. Professional services and agencies

Law firms, consulting practices, and engineering consultancies use job costing to measure what each engagement actually costs. Without it, billing rests on estimates that rarely hold.

Labour is typically the largest input. Billable hours are multiplied by the loaded rate for each team member, then supplemented by project expenses like travel or subcontracted work.

Over time, the data reveals which clients are genuinely profitable and which absorb more hours than the fee covers. That distinction rarely surfaces through gut feel alone.

Job Costing vs Process Costing

The two most common costing methods serve different types of operations. Understanding where each one fits helps you choose the right approach for your business, or know when to use both.

| Feature | Job Costing | Process Costing |

| What it tracks | Costs per individual job or project | Costs per production process or department |

| Best for | Custom work, unique projects | Identical units, continuous production |

| Cost assignment | Direct to each job | Averaged across all units |

| Industries | Construction, custom manufacturing, professional services | Food processing, chemicals, oil refining |

| Level of detail | High, per-job visibility | Lower, per-unit average |

| Complexity | More effort to track per job | Simpler allocation across volume |

Many businesses use both methods. A furniture manufacturer might use job costing for custom orders and process costing for standard catalogue items produced in bulk.

How to Calculate Job Costing

The job costing formula combines three cost categories. Each requires a different tracking method, but together they produce the full cost of delivering a job.

Total Job Cost = Direct Labour + Direct Materials + Applied Overhead

1. Labour costs

Calculated by multiplying the hours each worker spends on a job by their loaded hourly rate. That rate should include wages, superannuation, workers’ compensation insurance, and other costs required under Australian employment law.

Labour Cost = Hours Worked x Hourly Cost Rate

Take a carpenter working 40 hours on a renovation at a loaded rate of $65 per hour. The resulting labour cost is $2,600, before materials or overhead are added.

2. Material costs

Track all materials purchased or drawn from inventory for a specific job. Purchase orders, delivery dockets, or inventory requisitions are the most reliable way to assign these costs directly.

Material Cost = Sum of All Materials Consumed on the Job

On the same renovation, $4,800 in timber and $1,200 in fixtures come to $6,000. Add $600 in fasteners, and the total material cost reaches $6,600.

3. Overhead allocation

Overhead covers indirect costs that support all jobs but cannot be traced to a single one. Rent, utilities, insurance, administration, and equipment depreciation all fall into this category.

Applied Overhead = Overhead Rate x Cost Driver

To find the rate, divide total annual overhead by the chosen cost driver. If annual overhead is $180,000 and total labour hours are 6,000, the rate works out to $30 per labour hour.

For the 40-hour renovation above, applied overhead is $1,200. Total job cost comes to $10,400: $2,600 in labour, $6,600 in materials, and $1,200 in overhead.

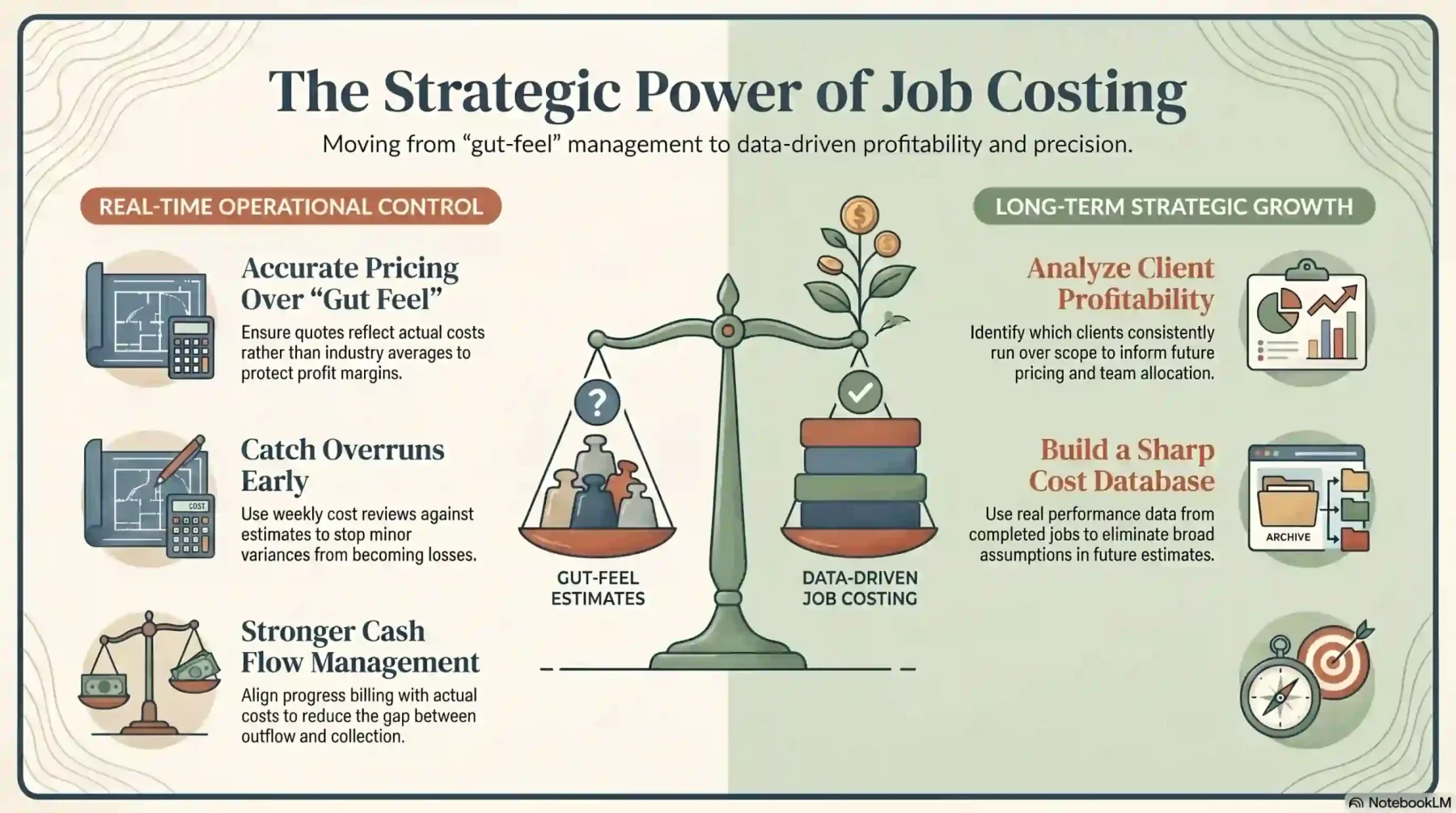

Benefits of Job Costing

Job costing does more than track numbers. When applied consistently, it gives businesses the visibility to price accurately, catch problems early, and build sharper estimates with every project they complete.

Accurate pricing: Job costing ensures quotes reflect actual costs rather than assumptions. This removes reliance on gut feel and industry averages, reducing the risk of underpricing and protecting margins on every job.

Early warning on overruns: Tracking costs against budget during the job, not after it closes, lets you intervene before a small variance becomes a significant loss. A weekly cost review against estimate catches drift early enough to act on it.

Client profitability insight: Job costing identifies which clients consistently run over scope and which stay within estimate. This informs how you price future work, how you allocate your team, and which client types are worth pursuing.

Stronger cash flow management: Progress billing tied to actual costs ensures you invoice proportionally to work completed, reducing the gap between cash outflow and collection.

Better estimating over time: Each completed job adds to your cost database. Over months and years, your estimates improve because they draw on real performance data rather than broad assumptions about what a job should cost.

Job Costing Example

To see how the formula works in practice, consider a plumbing contractor hired to complete a bathroom renovation. The job requires two plumbers working eight hours each across two days.

Each plumber is charged at a loaded hourly rate of $75, which covers wages, superannuation, and on-costs. Two plumbers at 16 hours each gives 32 total labour hours, costing $2,400.

Materials include $800 in copper piping, $1,400 in tapware and fixtures, and $300 in fittings and sealant. The total direct material cost comes to $2,500.

The business applies overhead at $25 per labour hour, based on $150,000 in annual indirect costs divided by 6,000 estimated labour hours. For 32 hours, that adds $800 in applied overhead.

Total job cost: $2,400 in labour plus $2,500 in materials plus $800 in overhead equals $5,700. If the contractor quoted $7,200, the job returns a gross margin of $1,500.

Common Job Costing Mistakes to Avoid

Even businesses with solid accounting habits fall into predictable patterns when tracking job costs. Knowing what to watch for reduces errors that quietly erode margins over time.

Skipping overhead allocation. Tracking labour and materials without allocating overhead understates true job costs. A job that looks profitable may actually break even or run at a loss once indirect costs are counted.

Using estimates instead of actuals. Relying on budgeted figures rather than real costs creates a gap between what you think a job cost and what it actually cost. Close each job with actuals to keep your records accurate.

Missing labour hours. Workers who forget to log time against a job leave a gap in the cost record. Even small gaps compound over multiple jobs and distort your view of where time is actually going.

Reviewing costs only after the job closes. Cost tracking that happens only at the end removes any chance to course-correct. Review costs mid-job so you can act while there is still time to recover margin.

Inconsistent cost codes. Using different codes for the same cost type across jobs makes reporting unreliable. Standardised cost codes let you compare performance accurately across your full job history.

How Job Costing Software Works

Manual job costing works for simple operations, but it struggles to keep pace as job volume grows. Job costing software connects the data sources that spreadsheets cannot manage reliably at scale.

When a worker logs hours against a job, the software applies the correct labour rate automatically. There is no manual calculation, and the cost appears on the job record in real time.

Purchase orders and supplier invoices are matched to specific jobs as they come in. Materials drawn from inventory are assigned directly to the job record, keeping material costs current without manual data entry.

Overhead is applied automatically using the rates you configure. As labour hours accumulate, the system calculates and posts overhead in the background, so total job cost stays accurate throughout the job lifecycle.

Reporting pulls everything together. You can view profitability by job, by client, or by project type across any date range, giving you the data to make sharper decisions about pricing, resourcing, and growth.

Conclusion

Job costing gives businesses the financial detail that broad accounting summaries cannot provide. Tracking labour, materials, and overhead at the job level reveals exactly what each project costs and where your margins come from.

For businesses managing multiple projects at once, the difference between guessing and knowing can be the difference between growth and margin erosion. Job costing software makes the process systematic and scalable.

To learn further regarding this topic, you can book a free consultation with us for free. Start today and expand your business.

Frequently Asked Questions

What is job costing in simple terms?

Job costing is a method of tracking how much it costs to complete one specific project. You record the exact labour, materials, and overhead for that job rather than averaging costs across all work.

What is the difference between job costing and process costing?

Job costing assigns costs to individual jobs and suits custom, project-based work. Process costing averages costs across a continuous production run and suits businesses that manufacture identical products at high volumes.

How do you calculate job costing?

Add direct labour costs, direct material costs, and applied overhead for the job. Labour equals hours worked multiplied by the loaded hourly rate. Overhead is applied using a predetermined rate tied to a cost driver such as labour hours.

Which industries use job costing?

Construction, custom manufacturing, professional services, legal firms, advertising agencies, and healthcare providers commonly use job costing. It suits any business that completes distinct, individually priced projects.

Can accounting software automate job costing?

Yes. Modern accounting and ERP software can pull labour hours from timesheets, match purchase orders to jobs, and apply overhead using preset rates. This removes the need for manual spreadsheets and reduces the risk of data entry errors.

![Balance Sheet Template: Free Downloads for Businesses [2026]](https://stg-cms.hashmicro.com/uploads/blog-5780aa690704-moneymoney-14.webp)