When production keeps running but margins keep tightening, the issue is often hidden in the cost per unit. Material usage, overtime, and overhead may rise quietly, while management only sees the impact after pricing and profit are already under pressure.

This matters as Malaysian manufacturers face cost pressure in 2026. According to FMM, elevated operating costs still constrain margins, while rising input costs remain the most cited challenge. Tracking production cost per unit helps management detect leakage earlier and respond faster to supplier, labour, or overhead changes.

Cost per unit is not only a finance number at month end. With manufacturing software for cost tracking, management can see where margins start leaking while production is still running, especially when purchasing, labour, overhead, and output data are not connected clearly.

Key Takeaways

|

When cost data is still slow to capture and harder to trust, production decisions become much more difficult to control. A more connected manufacturing system helps turn cost visibility into faster action before margin pressure gets worse.

What Is Production Cost Per Unit?

Production cost per unit is the total cost a manufacturer spends to produce one finished unit. It covers direct materials, direct labour, and manufacturing overhead, then divides the total by the number of units produced.

This number helps management see whether a product is still profitable after real production costs are counted. When the figure is inaccurate, pricing, margin review, and production planning can be based on assumptions instead of actual cost conditions.

Why Cost Per Unit Matters More When Margins Tighten

When margins tighten, production cost per unit becomes one of the clearest indicators of whether a product is still worth producing, repricing, or scaling. If this number is inaccurate, the business can keep pushing volume while actual profit continues to shrink. That is where manufacturers start making the wrong decisions, not because demand is weak, but because the real cost behind each unit is still unclear.

Higher output does not guarantee better margins

Higher output can look positive on paper, but it does not automatically improve margins. When scrap, overtime, utility usage, or rework increase along with production, volume can rise while profitability quietly weakens. Without accurate cost tracking, management may keep approving higher output that looks operationally strong but is already becoming commercially weaker.

Cost efficiency starts with better visibility

Better cost visibility helps teams track material, labor, and overhead more accurately for each unit produced. It also gives management a clearer basis for evaluating which work centers, product lines, or process changes are actually improving efficiency and which ones are only adding more cost without protecting margin.

Small cost changes can start the margin leak

A margin leak often starts from small cost changes that look harmless during production. Scrap increases slightly, overtime becomes more frequent, or material usage goes above plan. If these changes are not tracked by product or batch, management may only notice the problem after the margin has already dropped.

Where Margin Leakage Starts

Margin leakage often starts from small cost shifts like scrap, rework, overtime, or excess material usage. Because these issues build quietly while production still looks stable, the impact is often only noticed after profit has already come under pressure.

Small cost shifts often go unnoticed at first

Margin leakage usually does not start from one major mistake. It often begins with smaller cost movements that seem manageable at first, such as rising scrap, repeated rework, overtime dependency, or material usage that slowly moves above expectation. Because these shifts build gradually, they are easy to miss while production is still running and output still looks stable on the surface.

The damage often appears too late in financial reports

The bigger problem is that these cost movements are rarely visible early enough for management to respond. By the time the impact shows up in margin reports or monthly financial reviews, the business may already be absorbing weaker profit across several orders, product lines, or customer accounts. That is why stronger cost visibility matters, because management needs to see where margin starts weakening before the damage becomes harder to reverse.

What Makes Production Cost Per Unit Hard to Track

Production cost per unit is hard to track when material, labor, and overhead data sit in different places. Procurement may update prices, production may record usage manually, and finance may only confirm overhead at month end. This delay makes the real unit cost visible too late.

Material, labor, and overhead move separately

Material, labor, and overhead are often recorded by different teams, so the cost does not always connect to the right work order. Waste, rework, overtime, machine usage, utilities, and production overhead costs can make the real unit cost higher than planned if they are not allocated correctly.

Cost data updates too slowly

Cost data often arrives after production decisions are already made. When material prices, labor hours, or overhead changes are updated late, manufacturers may keep quoting or producing with outdated assumptions, allowing margin leakage to spread across orders or product lines.

Where Manual Cost Tracking Usually Falls Short

![]()

Manual cost tracking often looks manageable at first, but it becomes unreliable once production data starts moving faster than spreadsheets can handle. Purchase records, usage logs, and costing updates may all exist, but when they sit in separate files, the real cost per unit becomes harder to track accurately.

What looks like a reporting issue often becomes a business issue, because weak cost visibility leads to slower pricing decisions, weaker margin control, and delayed response when costs begin to shift.

Spreadsheet based costing lags behind production

Spreadsheets are still common, but they are too slow for production environments where costs can shift every day. Formula errors, duplicate versions, and delayed updates make it harder to trust the numbers, especially when product variants keep increasing. For management, that means cost review becomes backward looking, when what is actually needed is earlier visibility before pricing or production decisions are locked in.

Disconnected data hides real cost movement

Manual tracking also makes it harder to catch supplier price changes, scrap spikes, or production inefficiencies at the right time. This is where an integrated manufacturing ERP system becomes more useful, because operational and financial data can move together in one view. When cost movements are visible sooner, management has more room to adjust pricing, review product profitability, or intervene before leakage spreads further.

When Growth Starts Exposing Weak Cost Control

Cost control often looks manageable when production volume is still relatively stable and product complexity is limited. The pressure usually starts to show when output grows, more orders need to be handled at once, and cost movements become harder to monitor with the same level of accuracy. At that point, weak cost control stops being a reporting issue and starts becoming a business risk.

More volume creates more room for cost leakage

As production grows, cost leakage becomes easier to miss because scrap, overtime, rework, and indirect costs start increasing across more batches at the same time. Without stronger visibility, the business may continue scaling output while margin control becomes weaker underneath.

Growth is harder to manage without reliable cost visibility

When cost data is delayed or fragmented, management has less confidence in which products are still profitable, which orders deserve more capacity, and where efficiency is actually improving. This is why growth often exposes weak cost control faster, because the business needs stronger visibility to scale without losing control over margins.

What Manufacturing ERP Helps You Capture

A manufacturing ERP helps bring material, labor, and financial data into one connected view. Instead of relying on separate updates from different teams, manufacturers can track unit cost based on what is actually happening on the shop floor. This gives management a stronger basis for pricing, planning, and margin review because the numbers reflect current production conditions rather than delayed reconciliations.

Material consumption by order or batch

ERP systems can link material usage directly to a specific order or batch, making unit cost tracking more precise. If usage goes above the planned material structure, the variance can be seen earlier and reviewed before it affects margin further. That visibility is especially useful when management needs to know which batches are still efficient, which ones are absorbing too much material, and where waste is starting to weaken profit.

Work in progress and production activity

ERP systems also help track work in progress by recording material and labor activity throughout production. This makes it easier to see how much cost is building up in each order, especially when production runs across several stages or over a longer period. For management, this makes it easier to review whether production is still moving in line with expected cost, inventory value, and cash flow exposure.

Standard vs actual cost

Comparing standard cost with actual production cost helps teams see where efficiency starts to slip. When the gap is visible early, it becomes easier to trace whether the issue comes from downtime, rework, or higher labor usage. This matters because management can respond before cost overruns become recurring margin problems or start affecting pricing accuracy.

Better visibility over material usage, WIP, and cost variance gives management a clearer basis for protecting margin before the impact gets harder to control.

ERP Features That Support Better Cost Control

How Better Cost Tracking Improves Decisions

FAQ About Production Cost Per Unit

Why is production cost per unit important for manufacturers?

Production cost per unit matters because it shows whether a product is still protecting margin, whether pricing is still realistic, and whether higher output is actually worth scaling. When this number is unclear, management can keep pushing volume while real profitability continues to weaken underneath.

What makes production cost per unit difficult to track accurately?

It usually becomes difficult when material, labor, overhead, and financial data are recorded in separate systems or updated at different times. That gap makes it harder to see real profitability by product, batch, or order while production is still running, which delays response and weakens cost control.

How can a manufacturing ERP system improve cost visibility?

A manufacturing ERP system improves cost visibility by connecting production activity and financial data in one flow. This makes it easier to track material usage, compare standard and actual costs, review variances earlier, and reduce delays caused by manual reconciliation.

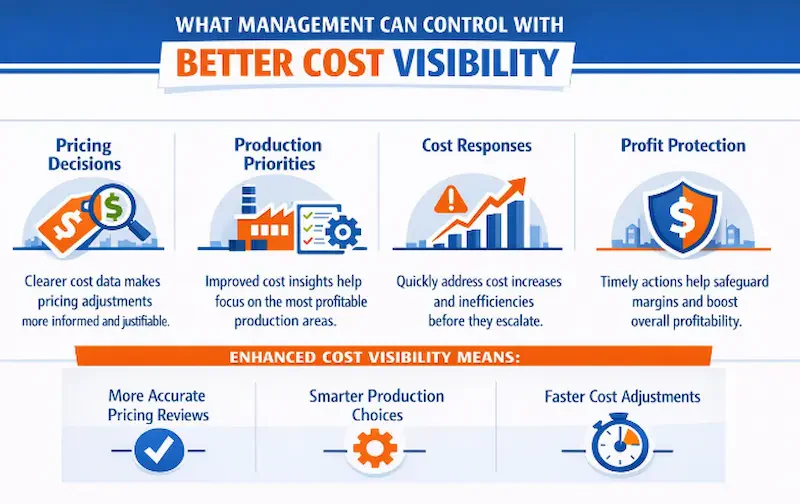

How does better cost visibility help management protect margins?

Better cost visibility helps management respond faster when costs begin to shift. It supports earlier pricing review, stronger control over waste and inefficiency, and better decisions on which products, orders, or production priorities still make commercial sense.

Can Management See Cost Pressure Early Enough?

Rising cost is not the only issue. The bigger risk is when management sees it too late to respond properly. When cost pressure is only visible after margins start falling, pricing, production priorities, and cost control become harder to adjust. Stronger visibility matters because it gives management more time to protect profit before the impact gets bigger.

How do you calculate production cost per unit?

To calculate production cost per unit accurately, make sure every cost comes from the same production period and the same output batch. The number becomes more useful when it includes actual material usage, labour time, rework, scrap, and overhead allocation, not just planned cost. This helps manufacturers see whether the final unit cost still supports the expected margin.